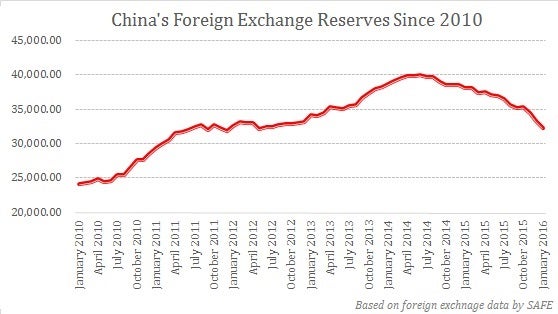

China’s hefty foreign exchange reserves got lighter by nearly $100 billion as the People’s Bank of China continued to support the yuan by selling dollars. According to the data by China’s central bank, the fall in forex reserves by $99.5 billion in January was lower than the monthly drop of $107.9 billion in December, which was the biggest on record.

The continued trend of selling of dollars by Beijing has taken its foreign exchange reserves to the lowest level since May 2012. However, despite a massive outflow of $513 billion during 2015, which was the biggest annual drop in history, China’s foreign exchange reserves at $3.2 trillion are still the world’s largest.

As announced on Nov. 30, 2015, the IMF board approved the inclusion of the renminbi in the Special Drawing Rights (SDR) basket as the fifth currency. On Oct. 1, 2016, renminbi (RMB) will join the US dollar, the euro, the Japanese yen and the British pound in the prestigious SDR basket of currencies.

The cooling down in asset prices, shaky stock markets and mild economic growth outlook for China has prompted investors to shift to dollar denominated assets at home and abroad, a process which has resulted in an abandonment of the renminbi. Further pressure has been added by companies looking to repay their foreign debt, as well as expectations of an interest rate hike by the Federal Reserve.

China's Grip on Currency

To stem the flight of capital, Beijing has put in place a number of mechanisms, from efforts to curb short selling and tapping currency speculation to the easing of foreign investment inflows into the mainland and selling dollars to support its currency.

China’s surprise devaluation of the yuan in August resulted in the first big drawdown for 2015, as forex reserves tumbled by $93.9 billion (and eventually the second biggest monthly fall for 2015). China has intensified its efforts to support its currency since the August devaluation.

China reported the slowest growth in 25 years during 2015 as its gross domestic product (GDP) expanded by 6.9%. Beijing has set its economic growth projection range at 6.5%-7% in 2016. According to Xu Shaoshi, Chairman of the National Development and Reform Commission (NDRC), “Downward pressure on the world's second largest economy will remain in 2016.”

China has always kept a tight grip on the way its currency moves, a practice which helped the mainland get over some of the worst periods of the global financial crisis, but its rigidity has relaxed over the years. Under the current account, the yuan is convertible for trade purposes, while the capital account, which covers portfolio investment and borrowing, is still largely state controlled to regulate sudden inflow and outflows. China recently relaxed the rules for investments for single institutions under its QFII program in order “to improve the convertibility of China's currency, the yuan, in the capital account and facilitate cross-border investment and financing,” according to the State Administration of Foreign Exchange (SAFE).

An analysis by Bloomberg Intelligence economists Fielding Chen and Tom Orlik on the question, “Does China have enough foreign-exchange reserves to defend the yuan?” says, “On the assumption that the country’s capital controls are effective, the IMF methodology requires it to hold reserves equal to 10% of annual exports, plus 30% of short-term foreign debt, 20% of other foreign liabilities and 5% of M2. That adds up to $1.8 trillion, which is well below the $3.3 trillion the PBOC actually held as of December. On that basis, even at the current rate of decline in FX reserves, China could defend the yuan for more than a year and still be in the IMF’s comfort zone.” It also suggests China’s capital controls are ineffective.

With the IMF methodology requiring China to have $2.9 trillion in reserves, $3.3 trillion may not be enough if the reserves continue to fall at the current pace, landing China below IMF’s red line by mid-2016.

The Bottom Line

China does have a challenging situation at hand. While the depreciation of its currency tends to boost export competitiveness, it further adds to capital flight from the mainland. Similarly, while the economic growth outlook suggests monetary easing, to do so would put pressure on its currency. Although China should be able to plug loopholes (like illegal foreign exchange activities) to curb the flight of capital while tightening capital control, a broader consensus is suggestive of a further gradual weakness in renminbi throughout 2016. However, a devaluation is not expected in near-term.

Blogger Comment

Facebook Comment